Banging My Head Against The Coin Laundry Market

As I analyze markets and industries from an investment perspective, I like to track my thoughts and learnings to ensure I get better at understanding different opportunities. For the last five years, I've been looking at laundromats around the SF Bay Area. I haven't bought any yet and I'm starting to wonder if I ever will. I hope you enjoy and get value out of my countless hours spent counting coins.

Overall Thoughts:

The minimal need for staff oversight led me to begin my initial research on Laundromats. Apart from a part time janitorial service and a handyman on call, there’s limited need to have others involved in this business. Many people spend 3-5 hours a week running these businesses which makes them attractive for operators with other full time jobs. Because of this, I spent my time thinking about traditional laundromats without any delivery services or other add-ons. One of my favorite things about Laundromats is the natural geographic monopoly that often occurs in this market. Due to the high start-up costs, it rarely makes sense for a new entrant to come into a market to compete with you. The market size is typically fixed (and declining in gentrifying neighborhoods) so you don’t often see irrational competition by an entrant focused on capturing the future growth.

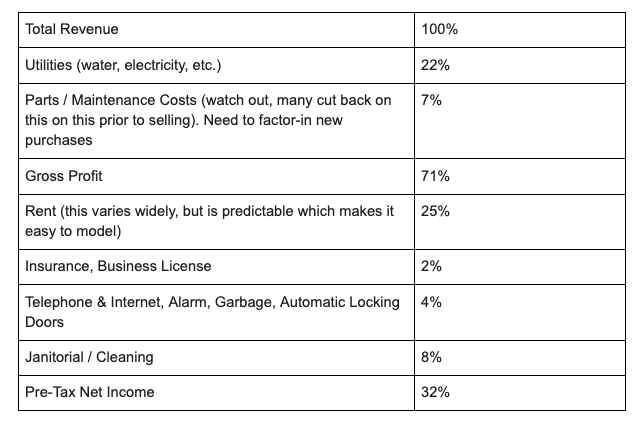

Margin Structure: This comes from a variety of sources who run laundromats and actually have to be honest.

Challenges / Important Factors to Research:

- Location, Location, Location: The location of your laundromat is everything. Your demand is 100% driven by where your laundromat is located and this is something you cannot change. It’s possible to slightly increase business through advertising, etc, but this will only drive a 5-10% revenue increase at most. When looking at laundromats, you should examine the demographics of the area (use common sense or public data) to understand income levels, likelihood of people needing washing machines and any changes in the neighborhood that are expected over the next 5-10 years. Gentrification is happening quickly in a lot of cities which can dampen the returns on your laundromat. You also want to observe competitors in the area that have the potential to take your business. How busy are they? Are they clean? Would you prefer that location over the one you’re buying?

- Utility Costs: Apart from maintenance on the machines, electricity and water are your largest variable expenses. These variable expenses are 100% out of your control which makes it a hard business to forecast and predict. In the last few years in San Francisco, the city has increased water costs by 10-15% twice. No owner wants to deal with a 30% increase in operating costs.

- Difficulty in underwriting: Because of the historical cash nature of this industry, accounting is terrible. Most owners are underreporting income and over-reporting expenses. The broker will often tell you this during early discussions, but it makes it nearly impossible to understand the financial picture of the business. I’ve found two ways of overcoming this: 1) Just underwrite the business based on the information they’ve provided. Hell, it’s kinda what they deserve after skimming the profits for so many years. 2) Ask for a video tape of the location or visit the location and make usage estimates based on observations. This is a time-intensive activity, and one I would recommend outsourcing if you have the financial means to make it happen. Another common method is determining the water usage per wash and then building a revenue model based on their water bill. Anyway you look at it, underwriting these businesses is hard. It often becomes harder as brokers can be shady and there is often a language barrier involved.

- Leases: Given the importance of lease terms on the financial profile of the investment (see above), it’s crucial to have favorable lease terms and have a good relationship with the landlord. I typically look for lease terms out ~10 years with built in extensions for 5 or 10 years. This provides a long-enough lead time that you can model these costs in and underwrite to a strong return. Also, always ask to meet the landlord face to face. This only serves to help.

- Rare, but Large Operational Headaches: One of the major advantages of this business model is the limited operational involvement. Apart from occasional maintenance issues that can be solved by external support, it’s a good opportunity for investors / owners who have other jobs. This is true 99.9% of the time, but in certain instances, there can be horror stories. Depending on the neighborhood, there can be homeless people trying to live in the location that need to be removed, crimes in the location, and people trying to steal things from the store. While most of this liability is resolved through having a security and video system, it still requires someone to deal with it.

- Machines: Having to replace machines can destroy a business and your returns from owning a business. It’s essential to get an independent maintenance review of the machines prior to purchasing a location so you can forecast if any machines will need to be replaced during your ownership period. New and used machines can be expensive, but many retailers offer financing services which lower the upfront cost of the machines.

Strengths / Value Creation Opportunities:

- Conversion from coins to credit cards: Many older laundromats still operate on coin-based systems. While good if you’re trying to avoid taxes (which I don’t advise), it’s a pain to operate these systems. You need to physically collect and count the coins and if you have employees handle this, there is always the risk of employee theft. In addition, a coin based system requires a bill to coin conversion machine since no one likes to carry around 100 quarters when doing laundry. These machines often break and require lots of trips to the bank. Moral of the story is that it’s a pain in the ass. You can replace these coin based systems with a system that accepts credit and debit cards at the machine and flows into an online platform that deposits the revenue and allows you to track the amount of business that your location is doing. This massively reduces the overall operational headache of owning the laundromat.

- Prepaid cards: While some of these new credit card machines still allow for the option to utilize quarters on each machine, the majority of the credit card machines eliminate the ability to accept quarters. While this is largely a positive, it may eliminate certain customers who are unbanked and don’t have access to a credit or debit card. The level of this will largely vary based on the demographics you serve. Most of these credit card machines allow for “prepaid” cards which operate on the gift card model where a customer can enter cash into a machine and receive a prepaid card to purchase laundry. This opens up your business to a wider customer set as previously discussed, but it also allows the owner to take advantage of the “gift card effect” in which a customer purchases $20 on the card, but only utilizes $15 on washes and then loses the card. The leftover $5 can be viewed as 100% margin revenue. While the ethics behind this technique can be viewed as questionable, I’ve seen laundromats massively benefit from this capability.

- Automatic doors: This one is a no brainer, but for around $1k, you can install automatic locking doors which eliminates the need for an employee (or you) to open and close the store on a daily basis. This allows for decreased operational headaches and wider operating hours which has the potential to increase revenue. From what I gather, there was some aversion to this in certain neighborhoods, but now it’s well utilized throughout the industry. If you come across an opportunity without these doors, there is a strong ROI to installing them since it lowers operating expenses from day one.

- Pricing Power: Since laundromats often operate as geographical monopolies, the business owner has the ability to raise prices without losing a large portion of the customer base. This is helpful in two situations: 1) when input costs increase. If water costs increase, you can typically pass 100% of the costs to the customer. 2) when you purchase a facility with prices well below market. In this situation, it makes sense to increase prices to the fair market level over time so as not to scare customers. In addition, owners should feel comfortable raising prices above inflation on an annual basis. These price increases become easier when you have a credit card or prepaid card model since the customer isn’t manually submitting quarters and all of the changes can be done via an online management platform.

- High Startup Costs: Only in rare cases, will it make sense for a new entrant to enter your market to compete with you. There are remarkably high start-up costs in the industry as new and used machines are expensive and finding a location that allows you to build out will be challenging. Through my research, I only heard about a few cases where this had happened.

- Recession Resistant: People need to do laundry in good times and in bad times. There is less risk of people spending money elsewhere because no one wants to smell bad. In addition, it's a small percentage of an individual's spending on a monthly basis so it's less likely to get cut.

Potential / Benefits to Scale: One of the challenges I’ve always had with the laundromat business is that it’s really difficult to grow the total value (enterprise value) of the business. Since revenue is driven by the number of machines and usage of machines, it’s impossible to meaningfully change the size and scale of the business without purchasing new locations or renovating your location. In addition, there are only so many people in a given area who need access to a laundromat so your market size is somewhat fixed (and I believed declining in my markets in California). All of this being said, there are some benefits to scale. Due to these challenges, I view investments in laundromats as a cash flow business that are attractive if you can secure a short enough payback period.

- Brand: I don’t buy this one, but one could argue that if you grow to multiple locations, your growing brand may attract new customers which increases the revenue of both locations.

- Synergies & Maintenance: Having multiple locations allows for shared services across the different locations. It’s easier to get better insurance, internet and other pricing discounts. However, these tend to be the smallest costs of these businesses which limits the upside potential. I think the largest potential synergy is for a business that scales to 5+ locations which allows them to hire a full or part-time maintenance person which would result in fewer breakdown and lower maintenance costs.

Typical Valuation & Returns: As I described earlier, I view Laundromats as a cash flow opportunity and I judge the attractiveness of a location by the payback period with a given level of business loss. Simply put, what will my cash flow return look like if my costs increase more than I expect and my customer base declines more than I expect. In these businesses with limited upside, you need to build a safety net to protect downside risk.

I’ve seen a wide range of valuations for these laundromats and they typically vary most by location (poorer communities have higher multiples due to confidence around customer base) and size of operation (more machines = more money).

When I put in offers, I was typically putting offers at 2-4x owners cash flow. It’s worth noting, I’ve seen fully upgraded laundromats sell for 4-8x owners cash flow which I’ve struggled to get comfortable with.

When I was underwriting these deals, I tried to aim for high teen (16-19%) cash flow return on equity (when using leverage) and high twenty (26-29%) cash flow returns after debt paydown. If I purchased a laundromat for $175,000 and funded $100,000 in equity and the remaining $75,000 with debt, I’d want to receive at least $16,000 in the initial years and at least $26,000 in later years after I’ve paid down the debt.